GOOD MORNING!

FOREX

The Dollar Index seems to be reacting less to rising crude and has chosen to remain stable around 101, which has led to strength in the Euro above 1.14. Yen to 162.66, Aussie above 0.70, and EURJPY above 186. However, we may expect the Dollar Index to test 100.70 before bouncing back towards 102 in the medium term, indicating that the above-mentioned strength in the currencies may be short-lived. EURINR looks bullish towards 110.50-111 while USDCNY can trade within 6.75-6.7850 for some time. Pound can test 1.33 while below 1.3550. USDINR has risen to close above 96.50 yesterday, which reduces chances of a fall to 96-95.85 and reinforces upside targets of 96.75-97.00. ECB policy meeting is due today, where markets expect the rates to be kept unchanged.

Dollar Index (101.062) tested 101.20 but has not been able to rise significantly despite the rise in crude prices. On the charts, there is scope for a dip to 100.70 before an eventual rise towards 102 or higher is possible in the medium term.

EURUSD (1.1417) has bounced back to trade above 1.14. The ECB is expected to keep rates unchanged today, while markets expect a rate hike in the Sep-26 meeting. With limited upside to 1.1470/1.15, the overall view looks bearish for a fall to 1.1350-1.13 in the medium term.

EURINR (110.2630) bounced from 109.70 itself, and while it sustains above 110, the pair can rise to 110.50-111 soon.

Dollar-Yen (163.05) has corrected a bit over yesterday and today and could pause for a few sessions while we see lack of rising momentum on the Dollar Index. Thereafter, the USDJPY could continue rising, targeting 164.50-165. Overall view is bullish.

EURJPY (186.17) has moved up on Euro strength above 1.14 and slight strength in the Yen. In the medium term, the pair looks bullish for a target of 187/188 while above 186.

USDCNY (6.7682) tested 6.7748 yesterday but has come off today, heading back to 6.76/75. We may expect fluctuation within the broad 6.75-6.7850 region for sometime till we see a decisive breakout from the range.

Aussie (0.7015) holds steady above 0.70 while the Dollar Index remains stable around 101. For the next few sessions at the least, we may expect Aussie to see a slow rise towards 0.7030/0.7050, but thereafter whether the rise will sustain or not needs to be seen.

Pound (1.3383) has immediate resistance near 1.3550-1.35 below which there is scope for a decline to 1.33 or even to 1.32/31. Unless a decisive break above 1.3550 is seen, the bulls may not take over the price action.

USDINR (96.5750) moved up to close higher above 96.50. This reduced our expectation of seeing a dip to 96-95.85 mentioned yesterday and reinforces bullish targets of 96.75-97.00 along with the rising Brent crude prices.

INTEREST RATES

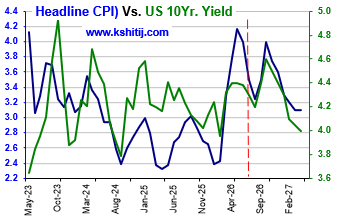

The US Treasury and the German Yields sustain higher. Both remain bullish and have room to rise more from here. The ECB meeting outcome today will need a close watch. The 10Yr GoI has risen back again. That still keeps alive the chances of seeing some more rise from here before the broader downtrend resumes.

The US 10Yr (4.65%) and 30Yr (5.14%) yields sustain higher. Our bullish view of seeing a rise to 4.7%-4.8% (10Yr) and 5.2% or even 5.35%-5.4% (30Yr) remain intact. Support is at 4.6% (10Yr) and 5.1% (30Yr).

The German 10Yr (3.17%) and 30Yr (3.65%) Yields remain stable but higher. The y can rise to 3.2%-3.25% (10Yr) and 3.75% (30Yr). Support is at 3%-2.98% (10Yr) and 3.55% (30Yr).

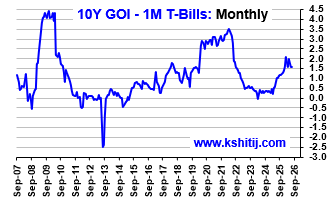

The 10Yr GoI (6.8012%) has moved above 6.8%. The chances are still alive to see 6.85%-6.9% before the overall downtrend resumes to see 6.7% and 6.6%.

STOCKS

Dow and DAX are likely to remain within the 52000-53000 and 24700-25500 ranges respectively. Nifty has turned weak after slipping below 24000 and needs to reclaim this level to revive the bullish outlook towards 24400; otherwise, it could decline towards 23800-23750. Nikkei has pulled back from key resistance and can fall further towards 65000-64000. Shanghai remains firm and can rise gradually towards 3900-3925.

Dow (52475.84, +0.05%) can continue to trade within the previously mentioned range of 52000-53000 for some time. However, with the ongoing tensions in the Middle East, the possibility of a break below 52000 cannot be ruled out.

DAX (25272.89, -0.01%) can continue to trade within the broad range of 24700-25500 while the support at 24700 holds.

Nifty (23,996.25, -0.79%) fell sharply and closed just below 24000 yesterday. It needs to rebound above 24000 to keep our earlier view of a rise towards 24400 intact. Otherwise, while it remains below 24000, there is a risk of a decline towards 23800-23750 over the coming week.

Nikkei (66760.69, +0.47%) pulled back from the resistance near 68000, as expected, and closed at 66450 yesterday. While this resistance holds, a further decline towards 65000-64000 can be seen.

Shanghai (3870.53, +0.09%) is inching up gradually and can rise further towards 3900-3925 in the near term.

COMMODITIES

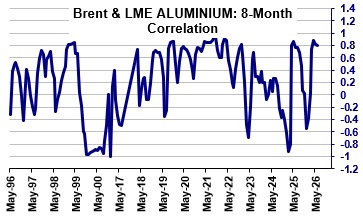

Crude prices remain strong, amid escalating geopolitical tensions. Brent and WTI can extend their rally towards $95 and $100 respectively. Gold is likely to remain within the broad $4000-$4200 range while below $4200. Silver can continue to trade within the $55-$65 range. Copper remains bullish despite the recent correction and can rise further towards $6.60-$6.70. Natural Gas has recovered and is likely to trade within the $2.80-$3.00 range for some time.

Brent ($95.73) and WTI ($88.16) are rallying in line with our expectations as the escalation of the US-Iran conflict has disrupted oil tanker traffic through the Strait of Hormuz, while threats by Houthi militants to blockade Saudi Arabia have further reduced tanker movement through the Red Sea. They can rise further towards $95 and $100 respectively in the near term.

Gold ($4124.66) is holding below $4200. While below this level, the broad range of $4000-$4200 could remain intact for some time.

Silver ($59.84) can continue to trade within the broad $55-$65 range for some time.

Copper ($6.51) has corrected slightly, but our view remains intact for a rise towards $6.60-$6.70.

Natural Gas ($2.9530) has bounced back, and a narrow range of $2.80-$3.00 could be be seen for some time.

DATA TODAY

1:30 07:00 Australia Labour Force

...Expected 15.2K ...Previous 40.3K

11:45 17:15 ECB Mtg

...Expected 2.40 % ...Previous 2.40 % -

DATA YESTERDAY:-

--------------

UK CPI Y/Y

...Kshitij Expn 2.40 % ...Expected 2.70 % ...Previous 2.89 % ...Actual 2.59 %

DISCLAIMER

These views/ forecasts/ suggestions, though proferred with the best of intentions, are based on our reading of the market at the time of writing. They are subject to change without notice.Though the information sources are believed to be reliable, the information is not guaranteed for accuracy. Those acting in the market on the basis of these are themselves responsible for any profits or losses that might occur, without recourse to us. World financial markets, and especially the Foreign Exchange markets, are inherently risky and it is assumed that those who trade these markets are fully aware of the risk of real loss involved.

WARNING !!

Visitors should be aware that Foreign Exchange transactions and trading are or can be subject to laws, rules and regulations of the country in which the entity undertaking the transactions is situated. It is incumbent upon the Visitors to keep themselves informed and abreast of the Laws they are (or would be expected to be) subject to and governed by, and act in accordance thereto.