GOOD MORNING!

FOREX

The Dollar index surged to 100.109 after US NFP data came out higher than expected on Friday, posting 172k and thereby raising chances of a rate hike by the FED. But we may expect a dip from anywhere between 100.10-100.50. Euro can bounce back while above 1.15 to prevent further decline to 1.14. EURINR and EURJPY have risen from Friday’s lows and have scope to rise in the near term towards 111 and 185/185.25, respectively. USDJPY continues its slow uptrend while USDCNY may rise to test 6.80/83 before facing rejection from there again towards 6.77. Aussie and Pound can rise to 0.71 and 1.34+ from current levels. USDINR fell sharply on positive measures by the RBI and the Indian government to induce foreign capital inflow, but whether that weighs over the overall strength in the US Dollar will have to be seen. But we may expect a higher spot towards 95.25/30 at least, if not more.

Dollar Index (100.13) rose exactly as expected triggered by a strong US NFP data release on Friday. As mentioned, we may expect an immediate dip from the 100.10-100.50 region, limiting its immediate rise further and dragging it towards 99.50 but it is to be seen if it can rise back towards 101 in the medium term.

EURUSD (1.1520) also dipped after breaking below 1.1575, as mentioned on Friday. The price may hold above 1.15 and bounce back towards 1.16 soon. Failure to bounce from 1.15 would open up chances of a decline to 1.14.

EURINR (110.1503) too fell sharply to 109.3854 as Euro declined. But the pair seems to have recovered today. However, rise in the Euro today, if seen today, can take the cross price higher.

EURJPY (184.69) has bounced from Friday’s low of 184.499 and could have scope to test 185-185.25 before either breaking higher or pausing for a reversal from there.

Dollar-Yen (160.31) continues to hold on to its slow upmove and could target 160.50-161 soon.

USDCNY (6.7829) has moved up well on strong US Dollar. But the immediate rise is expected to be limited to 6.80/83 before we see another decline towards 6.77 or lower in the medium term.

Aussie (0.7047) fell sharply to levels below 0.71 and while that holds, there is a chance of seeing a test of 0.69 or slightly lower. Else a bounce back to 0.71+ can be seen soon.

Pound (1.3337) has immediate support at 1.33 above which the price is likely to be bullish towards 1.34.

USDINR (94.95) fell sharply and closed lower on different measures by the RBI and the government to attract foreign capital inflows. But it is important to see if the pair could open higher today and move up due to the strong US Dollar. Domestically positive news on Friday and overall Dollar strength together could limit a sharp rise in the USDINR but we may expect a rise towards 95.25/30 at the least today.

INTEREST RATES

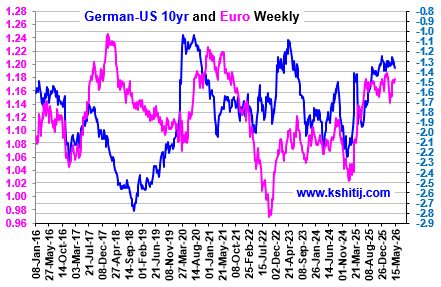

The US Treasury Yields have risen sharply after strong jobs data release on Friday increased the hopes for a rate hike. The US NFP rose by 172K (Market Expectation: 95K) and the unemployment rate remained stable at 4.3% The rise is getting support from oil price rise in the early trades today. A break above the immediate resistance can boost the momentum and take the yields higher. The chances of the fall indicated last week have been negated. The German yields are struggling to get a strong follow-through rise. That keeps them vulnerable to fall from here. We will have to wait and see. The 10Yr GoI has dipped further. It can fall more in line with our expectation before reversing higher.

The US 10Yr (4.56%) and 30Yr (5.02%) Treasury yields have risen sharply. A break above 4.6% (10Yr) and 5.05% (30Yr) will boost the momentum for a rise to 4.8% (10Yr) and 5.2% (30Yr) thereafter. The chances of breaking below 4.45% (10Yr) and 4.95% (30Yr) has been negated.

The German 10Yr (3.04%) and 30Yr (3.57%) yields is struggling the get a strong follow-through rise to clear the way for 3.1%-3.2% (10Yr) and 3.65%-3.7% (30Yr). That keeps it vulnerable for a fall to 2.9%-2.85% (10Yr) and 3.45% (30Yr). We will have to wait and watch.

The 10Yr GoI (6.9772%) has dipped further. That keeps intact our view of seeing 6.9% on the downside.

STOCKS

Global equities remain under pressure. Dow and DAX are weakening in line with expectations and can decline further towards 50500-50000 and 24250-24000 respectively. Nikkei has fallen sharply amid Middle East uncertainty and higher interest rate expectations, with scope for a further decline towards 63000. Shanghai also remains weak below 4000 and can fall towards 3900-3850. Nifty is relatively resilient and can rise towards 23,600 while holding above 23,200.

Dow (50797, -0.31%) has turned sharply lower due to stronger-than-expected US jobs data. A further decline towards 50500-50000 remains likely in the near term.

DAX (24572.36, -0.93%) is falling in line with our expectations and has tested a low of 24381. A further decline towards 24250-24000 can be seen in the near term.

Nifty (23,366.70, -0.21%) can rise towards 23,600 in the near term while it holds above 23,200.

Nikkei (64250.46, +0.02%) fell sharply by 5.20% on Friday due to uncertainty in the Middle East and expectations of higher interest rates. A further decline towards 63000 can be seen in the near term.

Shanghai (3989.89, +0.08%) opened lower with a gap down at 3938.70 today, and while below 4000, a further decline towards 3900-3850 can be seen.

COMMODITIES

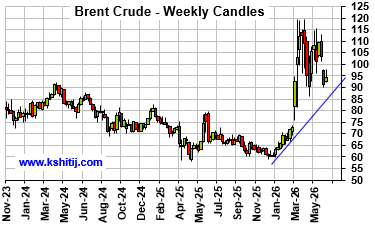

Crude prices have opened higher after Friday's decline, and the broader outlook remains positive for a rise towards $100 in the coming weeks. Gold and Silver have turned sharply weaker following stronger-than-expected US jobs data and can decline further towards $4300-$4200 and $65-$60 respectively if current weakness persists. Copper has broken below key support and may fall towards $6.20-$6.00. Natural Gas has pulled back from recent highs, but the downside appears limited to $3, with a broader $3-$3.50 range likely to hold for some time.

Brent ($96.39) and WTI ($93.77) closed lower on Friday but have opened higher today. We retain our view of a rise towards $100 in the coming weeks.

Gold ($4336.40) has broken below $4400, contrary to our expectations, due to a stronger-than-expected US jobs report, which has boosted the Dollar. If the price sustains below this level, a further decline towards $4300-$4200 remains likely.

Silver ($67.70) has dropped sharply below $70 due to stronger US economic data. It can decline further towards $65-$60 if it sustains below $70.

Copper ($6.28) has broken below the mentioned support and can decline further towards $6.20-$6.00 if the weakness persists.

Natural Gas ($3.1750) has retreated from Friday's high of $3.3650. The downside could be limited to $3, and a broad range of $3-$3.50 could hold for some time.

DATA TODAY

NO MAJOR DATA TO BE RELEASED TODAY

DATA LAST FRIDAY

================

GMT 4:30 IST 10:00 RBI Repo Rate

...Market 5.25 ...Previous 5.25 ...Actual 5.25

GMT 4:30 IST 10:00 RBI Rev Repo Rate

...Previous 3.35 ...Actual 3.35

GMT 4:30 IST 10:00 RBI MSF

...Previous 5.50 ...Actual 5.50

GMT 9:00 IST 14:30 EU GDP

...Market 0.1 ...Previous 0.1 ...Actual -0.2

GMT 12:00 IST 17:30 IN GDP

...Kshitij 7.7% ...Market 7.2% ...Previous 7.8%

GMT 12:30 IST 18:00 US NFP

...Kshitij 76 ...Market 95 ...Previous 115

GMT 12:30 IST 18:00 US Unemployment Rate

...Market 4.3 ...Previous 4.3

GMT 12:30 IST 18:00 US Avg Hrly Earnings

...Kshitij 0.4 ...Market 0.3 ...Previous 0.2

GMT 12:30 IST 18:00 US Average Hourly Earnings Production & Non Supervisory Employees

...Previous 0.3

{GMT 12:30 IST 18:00 CA Labour Force

...Market 10.20 ...Previous -17.17

DISCLAIMER

These views/ forecasts/ suggestions, though proferred with the best of intentions, are based on our reading of the market at the time of writing. They are subject to change without notice.Though the information sources are believed to be reliable, the information is not guaranteed for accuracy. Those acting in the market on the basis of these are themselves responsible for any profits or losses that might occur, without recourse to us. World financial markets, and especially the Foreign Exchange markets, are inherently risky and it is assumed that those who trade these markets are fully aware of the risk of real loss involved.

WARNING !!

Visitors should be aware that Foreign Exchange transactions and trading are or can be subject to laws, rules and regulations of the country in which the entity undertaking the transactions is situated. It is incumbent upon the Visitors to keep themselves informed and abreast of the Laws they are (or would be expected to be) subject to and governed by, and act in accordance thereto.