GOOD MORNING!

FOREX

The Dollar Index rose sharply above 106, contrary to seeing a fall towards 105 and it is now likely to head towards 106.5-107. Meanwhile, the Euro is expected to test the support at 1.06. EURJPY continues to trade within 165-162 region while USDJPY failed to sustain above 154.80 and can now decline towards 153/152 soon. Aussie and Pound have declined below their respective supports and are likely to test 0.63 and 1.23 respectively. USDCNY has risen past 7.24 but could face rejection around current levels else can test 7.25. EURINR could rise towards the upper end of the 88-90 range. In USDINR, we need to be cautious around 83.50/55. Break above 83.55 will take it towards 83.60/70.

Dollar Index (106.285) reversed from 105.74 itself and moved above 106, contrary to our expectations of seeing a fall towards 105. While above 106, a test to 106.5-107 looks likely.

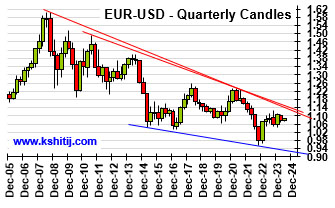

EURUSD (1.0618) fell sharply from 1.0690, holind below 1.07 and could re-test 1.06 in the near term , keeping a sideways range of 1.06-1.07 for a while. thereafter a break on either side would decide the further course of direction.

EURJPY (163.29) held well below the resistance at 165. An immediate range of 165-162 may hold for the next few sessions.

Dollar-Yen (153.87) had been ranged over this week, unable to rise past 154.80. The current fall may extend towards 153/152 with upside limited to 155 in the near term.

USDCNY (7.2420) has risen past 7.24, contrary to our expectation of seeing a range of 7.22-7.24 for a while. The current upmove can take it higher towards 7.25 but thereafter, only a decisive break past 7.25 can make the outlook bullish for the medium term.

The expected rise in Aussie (0.6375) to 0.65/6550 did not happen and instead, it started to decline towards 0.63 much earlier than anticipated. We expect the downside to be limited to weekly support at 0.63 and see a medium-term rise towards 0.64-0.65 again.

Pound (1.24) is declining as expected and could soon test 1.2350/23 on the downside.

USDINR (83.5425) has managed to close above 83.50 and has a fair chances of rising further towards 83.60/70 if it sustains above 83.50. The immediate view is bullish above 83.50.

EURINR (88.8730) has declined a bit but while above 88/88.50, we are keeping our view intact to see a rise towards 90. We expect the 88-90 range to hold for now.

INTEREST RATES

The US Treasury yields have inched. The bias remains positive to see more rise from here. Need to see if a strong follow-through rise is happening from here or not. The German yields have just broken their range on the upside. While the breakout sustains, a further rise is possible. The 10Yr and 5Yr GoI remains bullish and have room to rise more from here.

The US 10Yr (4.61%) and the 30Yr (4.72%) yields have inched up slightly. If the 10Yr sustains above 4.6%, a rise to 4.75%-4.8% is possible and that will avoid falling back to 4.4%. The 30Yr can test 4.8% and the price action thereafter will need a watch.

The German 10Yr (2.49%) and the 30Yr (2.62%) yields have just broken their 2.2%-2.45% (10Yr) and (2.4%-2.6%) range on the upside. While this sustains, a rise to 2.6% (10Yr) and 2.75%-2.8% (30Yr) can be seen in the coming days.

The 10Yr GoI (7.1905%) and 5Yr GOI (7.1957%) have risen back well. Bullish outlook is intact. The 10Yr can break 7.2% and rise to 7.3%. Supports are at 7.16%, 7.14% and 7.1%. The 5Yr can rise to 7.3% and even 7.4%.

STOCKS

Dow Jones is stuck in a narrow range below 38100 but remains vulnerable to a fall in the near term. DAX has bounced slightly but outlook will remain bearish as long as it holds below 18000. Nikkei continues to fall and looks bearish to test 36000 before a bounce can be seen. Nifty closed lower just below its key support and a further fall below 21900, if seen, will intensify the sell-off. Shanghai remains bullish to see a break on the upper end of the sideways range and target further upside.

Dow (37775.38, +0.06%) is stuck between 37600 and 38100. The bias is negative to see a fall to 37200-37000 while below 38100.

DAX (17837.40, +0.38%) has bounced back slightly. But while below 18000, the view is bearish to see 17400 on the downside.

Nifty (21995.85, -0.69%) has closed just below 22000. A fall below 21900 will intensify the sell-off and drag it down to 21500-21300. The price action and the weekly closing today could be important.

Nikkei (36770.50, -3.37%) has declined sharply below 37000. A test of 36000 looks possible before a bounce back can happen towards 38000-38500.

Shanghai (3072.78, -0.05%) rise to 3102.55 yesterday and has come down a bit from there. For now, the 3000-3100 range remains intact. Bias is positive to see a break on the upside and rise towards 3150-3200 in the coming days.

COMMODITIES

Strong recovery is seen in Crude prices due to geopolitical tensions between Israel and Iran. Gold and Copper have scope to test their immediate resistance before a corrective fall can happen. Silver looks ranged but has potential to rise while above the support at 28.00-27.50. Natural Gas looks bullish within its 1.50-2.00 sideways range.

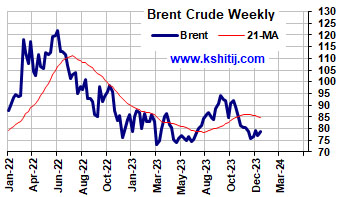

Brent ($90.38) tested $86.09 in line with expectations for a test of $86-85 and has bounced back sharply above $90. A rise towards $92.50-93.00 looks possible.

WTI ($85.29) bounced back after testing $81.06. We had expected to see a dip to $80. The bounce can extend up to $88-90.

Gold (2424) has moved up towards 2435. A rise towards 2450-2500 or even 2520 looks possible. After that, a corrective dip might be seen towards 2400.

Silver (28.79) looks ranged within 28-29. However, chances of rise towards 30.00 will remain intact while it stays above 28.00-27.50.

Copper (4.4640) is heading up towards 4.50 in line with expectations. 4.50 is a key immediate resistance. While that holds, a corrective dip towards 4.35 can be seen.

Natural Gas (1.7780) continues to rise and might head towards 1.9. A broad sideways range of 1.5-2.00 is expected to hold for the near term.

DATA TODAY

23:30 05:00 JP CPI

...Kshitij Expn 2.7 ...Expected - ...Previous 2.8

Data Yesterday

............

1:30 07:00 Australia Labour Force

...Kshitij Expn - ...Expected 7.2K ...Previous 117.6K ...Actual -6.6

12:30 18:00 US Philifed Index

...Kshitij Expn - ...Expected 0.8 ...Previous 3.2 ...Actual 15.5

14:00 19:30 US Existing Home Sales

...Kshitij Expn 4160K ...Expected 4200K ...Previous 4380K ...Actual 4190K

DISCLAIMER

These views/ forecasts/ suggestions, though proferred with the best of intentions, are based on our reading of the market at the time of writing. They are subject to change without notice.Though the information sources are believed to be reliable, the information is not guaranteed for accuracy. Those acting in the market on the basis of these are themselves responsible for any profits or losses that might occur, without recourse to us. World financial markets, and especially the Foreign Exchange markets, are inherently risky and it is assumed that those who trade these markets are fully aware of the risk of real loss involved.

WARNING !!

Visitors should be aware that Foreign Exchange transactions and trading are or can be subject to laws, rules and regulations of the country in which the entity undertaking the transactions is situated. It is incumbent upon the Visitors to keep themselves informed and abreast of the Laws they are (or would be expected to be) subject to and governed by, and act in accordance thereto.